Version française/French version: LINK

E. Krieger

One of the best-kept secrets of the Republic is that very few people can read a company’s financial statements, even though these reports are much less complex than learning a foreign language. How can we explain this mystery?

This paradox is a boon for financial experts. In the land of the blind, it is true that the one-eyed are kings; thus, the ability to interpret a balance sheet and forecast accounts will make you a high-flying pilot.

This lack of financial literacy is even present among some finance executives who believe that a company’s performance can be measured simply by revenue and net profit, even though these indicators reveal nothing about your capacity to generate sufficient operating cash flow for growth.

Profitability Alone Isn’t Enough

Indeed, profitability alone is not always sufficient if you want to grow through self-financing, especially if this growth also requires significant investments (Capex) and a high working capital requirement (WCR), whose increase can absorb most of your self-financing capacity.

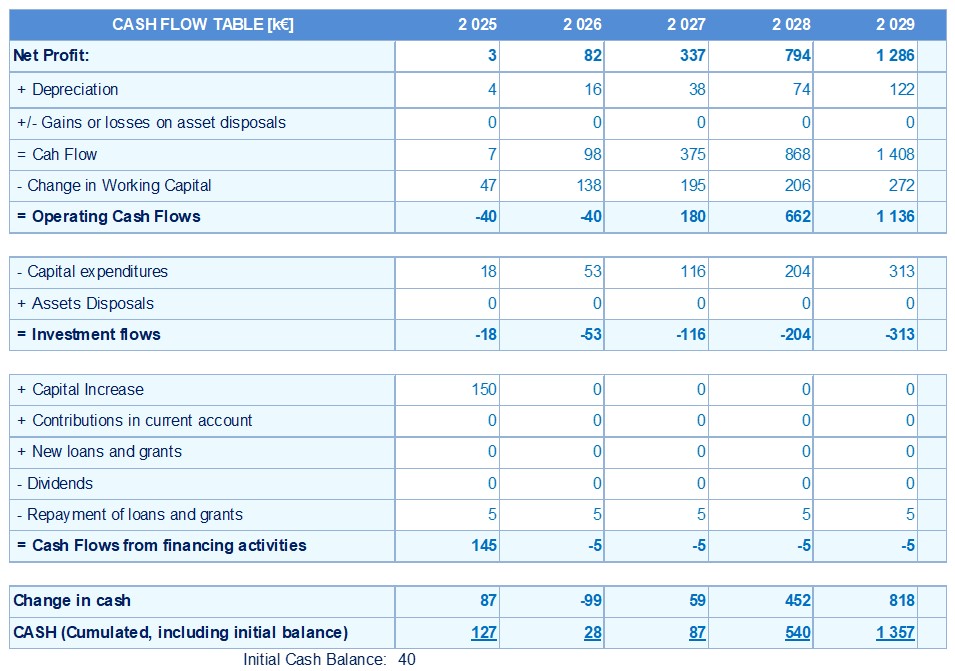

I served on the board of a publicly traded company where the CFO provided us with a host of charts and enlightening ratios. However, a venture capital fund representative continually requested a summary table from this CFO, one that would allow for precise monthly cash flow monitoring through:

- Operating cash flows

- Investment flows

- Financing flows.

‘Nothing is created, nothing is lost, everything is transformed,’ said Antoine Lavoisier, a brilliant chemist and financier of the Enlightenment. Ultimately, the evolution of your cash flow results from these three types of flows.

Like the Plitvice National Park in Croatia, with its terraced lakes connected by waterfalls and streams, the flow of the lower river results from the upstream flows.

This brings us to the saying: ‘Sales is vanity; profit is sanity; cash is reality.’

Ignorance and/or Power Games?

Incantations make no difference: you can’t pay bills with words.

Even 40 years ago, my professors at HEC were denouncing the harms of detached cost accounting, which makes it possible to make seemingly profitable activities appear unprofitable and, conversely, to allow value-less and impact-less offers to continue.

It seems that after all these years, these psychedelic practices and/or power games persist, even in prestigious companies overly influenced by controllers or managers who have often never sold anything in their lives. When we forget that mainly clients and fund providers pay salaries every month, the wake-up call can be painful.

An Example of Dysfunctional Injunctions

For example, a weekly target of 20 daily sales at €450 per unit corresponds to €9,000 net per day. If the average payment terms are one month and the gross margin of this product or service is two-thirds (67%), this translates into a daily margin target of €6,000.

This revenue goal can also be reached with 10 sales of a ‘premium’ offer at a unit price of €900. If these sales are made on a cash basis with a gross margin of 80%, this would generate €7,200 per day, or 20% more than the previous margin, with half the products and no working capital requirement.

A child would understand this basic reasoning. And yet some managers insist on requiring a quota of 20 daily sales, regardless of the product’s price, margin, and payment terms.

Other fans of alternative realities and ‘creative’ cost accounting will try to persuade you to maintain offers that don’t meet your criteria. This is pure schizophrenia, like if a multi-brand dealership asked a Ferrari Roma seller to match the sales volume of a Fiat 500 seller.

What to do in this case? The answer is simple: return to cash flow.

Recommendations for Entrepreneurs and Financial Managers

To facilitate rational exchanges, here are two simple recommendations to help you speak the same language within your company… and benefit from your differences:

Entrepreneurs and executives: educate yourselves! When you know how to read your company’s financial statements, you’ll be able to steer it much more effectively and can refute those who claim that some ‘cash cow’ activities are unprofitable.

Finance professionals and functional managers: develop real indicators! In other words, go all the way with the profit equation and implement a management information system based on cash flow.

This will help curb the debilitating power games that persist in so many organizations that have forgotten the fundamentals of creating and sharing value.

The Essential Financial Language

Accounting is a rather tedious discipline, but it’s essential for making economic and financial arguments.

Indeed, unlike certified illusionists and fans of detached cost accounting, you can’t pay bills with words—unless you’re a bestselling novelist or a talented lyricist like Claude Lemesle.